Dear Investors,

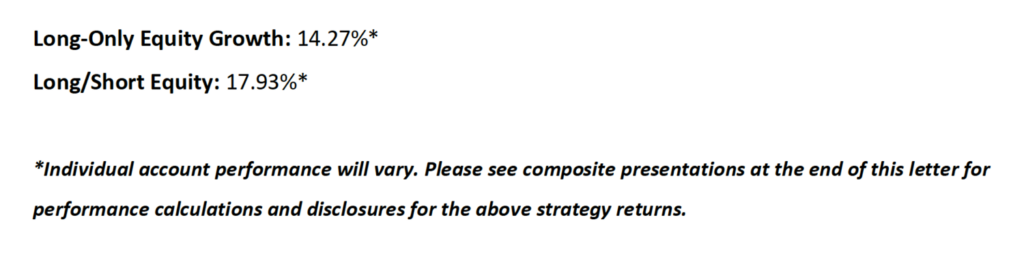

In Q1, 2018, our strategies produced the following results:

Please see here for composite presentations for additional information and disclosures.

If you’ll give me a few moments of your time, I’d like to share with you some insights and ideas about the market over the last few months and our strategy over the years to come. In short, these are exciting times for us at Nightview Capital—and the amazing part is that I feel like we’re just getting started.

Over the last few years, it’s been my credo that it’s a fantastic time to be a stock picker. And I truly believe it is. As I update our valuation models on a go-forward basis, I see compounded growth and fantastic opportunity ahead. In my opinion, our roadmap going forward is just as strong—if not stronger—than the previous five years.

Alternatively, there are plenty of potential value traps in the market today, if one applies limited valuation models. Many short-sighted models focus nearly exclusively on previous earnings, compounded out at some basic growth rate. But because of market disruptions, we believe those growth rates for many companies may turn negative in the near future. As a result, we believe earnings at many legacy companies could potentially evaporate in a far shorter time period than the market has currently priced.

From a business perspective, we believe the companies comprising our long positions are winning over clients with dominant “value propositions” that could allow for solid growth, even in a market slowdown. All our valuations are based on future cash flow projections, brought back to a present value. The valuation of each company in our portfolio requires a highly detailed and in-depth analysis of the business, along with its prospects going forward—with a margin of error included. All potential avenues must be explored to ensure that the current valuation remains below an “intrinsic value.” And before any capital is committed, we must have an extremely high level of confidence in each investment opportunity.

Successful long-term performance requires diligence, ability to focus on what really matters, and a willingness to constantly challenge your assumptions. While we experienced some volatility at the end of the quarter, which we expect to happen from time to time, we remain very pleased with our YTD performance. Of course, there has been some hysteria in the marketplace over the last quarter, and I will address that below. But most importantly, despite political frenzy and headline noise, we believe that our portfolio companies remain in great position going forward.

As I have written before, we anticipate a massive redistribution of wealth in our five research verticals (Cloud computing, Transportation, Energy, Content, and Retail). We believe this redistribution provides us with a world of opportunity going forward, on both the long and short side of our books. We look forward to continually monitoring the portfolio and maintaining discipline in capital allocation in our unique research verticals going forward.

•••••

Investing in disruption: The Nightview Capital “playbook”

Nearly six years ago, I revamped my investment strategy based on a simple but exhilarating premise: Technological disruption is radically redefining the American economy—and we want to participate in this “revolution.” Cars are going electric. Retail is moving online. Information technology is migrating to the cloud. I’ve said it before, and I’ll say it again to underscore the point: For investors, we believe the market environment is ideal. Business change is not only massive, but it’s happening at breakneck speed.

These sorts of paradigm shifts do not happen often, and they do not happen overnight—but when they come, they can come like a tsunami. We liken current disruption to a “Cambrian explosion”—a time for radical reshaping and consolidation.

By the end of the next fiscal quarter (June 30, 2018), our Equity Growth strategy will complete its sixth year. Since the strategy inception, it has annualized 25.53%* as compared to 14.59% for the S&P 500 Total Return index over the same period.

Our Long/Short Equity strategy completed it’s first year of performance as of the end of February and has returned 25.62%* annualized since inception as compared to 12.97% for the S&P 500 Total Return Index over the same period. We are very excited by the current and future opportunities we seek to capitalize on with this strategy going forward.

*annualized performance is based upon calculations contained in the composite presentation.

•••••

What’s happening in the market—and our approach

What happened this quarter? Unless you’ve been hibernating for winter, you’ve probably noticed a fair bit of volatility. February is traditionally a somewhat sleepy month, but not in 2018. Despite being the shortest month of the year, the Dow experienced not one, but two 1,000-point plunges. Then, in March and early April, the market reacted swiftly to the President threatening an international trade war, as well as tariffs on Chinese imports. There was also a good amount of non-fundamental trading with large price movements.

Protectionist trade policies cause a fair amount of nausea for day traders—but for us, as long-term investors in disruptive technology—we don’t believe it is material over the long haul. While stock prices can be volatile, the intrinsic value of businesses changes very little day to day and we are first and foremost buying equity in a business for the long-term. Our businesses grew during the quarter and we believe have improved their positions going forward. The nature of markets is unfortunately not linear, but if we look at the performance of our individual positions YTD we feel highly comfortable with a pullback.

While we always monitor political risks, in our view, the current rhetoric coming from Washington is more bluster than anything else, particularly regarding the President’s threats directed at Amazon. We will continue to monitor—and adjust if necessary—but we have seen these sorts of threats in different forms before, and we believe Amazon is on solid footing (See: BLOOMBERG: “Amazon and Bezos can’t be hurt by Trump”). We did close out our small position in Facebook early in the quarter, so we were unaffected by Facebook’s recent turmoil.

As I noted in my previous Partner letter, in the last 90 years, 2017 was the first time where the S&P 500 did not post a negative monthly total return. That is remarkable—so it’s not particularly surprising to me that February finally broke that streak with March following in the red. And to that I say: Good. I have no expectations that the exuberance of this bull market will continue forever.

But with that possibility in mind, in our long/short equity fund we have strategically built out our short book in recent months to hedge against negative downturns in the overall market while also seeking to capitalize on negative company specific events/trends—and I’d like to share a bit of our selection process to build out this portfolio.

•••••

Retail apocalypse—the ups and downs

Specifically, our short book philosophy is based on an inverted idea of disruption: That over the long- term, the incumbent business models could be too slow to adapt to changes in their categories, they could lose customers, and the value of their business may decline. In Q1 2018, we have strategically screened and sought out over a dozen companies to add to the short portfolio. All of these companies fall within verticals that face significant disruption—ranging from brick and mortar retailers to legacy IT businesses that we believe have not moved swiftly enough to adapt to a new cloud environment.

From a macro perspective, the companies we generally seek to short are highly leveraged with weak cash positions, unsustainable levels of debt, and management that, we have determined, are more concerned with balance sheet maneuvering and financial engineering than investing in products and services that will win customers now and into the future.

In particular, our short positions focus on legacy retailers that are being disrupted by what we believe is Amazon’s vice-like grip of the e-commerce market. Our position is that Amazon’s chokehold on these companies is strengthening and staggering—and we expect to retain these short positions in our portfolio, albeit with tight stops to limit our risk and exposure to occasional upswings and volatility.

In the last few months, we have continued to conduct deep-dive research into national retail data. The results have painted a damning portrait of what’s happening to brick and mortar shops in America: According to data firm One Click Retail, Amazon is now responsible for about 44% of all U.S. e- commerce sales last year, and four percent of all retail in America. We believe these percentages will likely increase over time as Amazon continues its foray into new segments, such as car parts, consumer electronics, and home and kitchen items. (If you have read any of my previous columns, of you have likely seen me write about “winner take all” environments—this is how it looks in the wild.)

Going forward, we believe Amazon will continue to pose a potential existential threat for brick and mortar retailers. And there’s a simple reason why: Amazon can provide a better price, product and service for the customer. This past quarter, you have likely seen the news that Toys R Us is liquidating all 735 stores nationwide. But nationwide, many more stores will be closing up shops—and we’ve been tracking the massive decline.

An estimated 7,795 U.S. retail store closures were announced in 2017, according to a research note from UBS, setting a new record. More will come. In 2018, Foot Locker will close 110 stores, Abercrombie & Fitch will close 60 more stores, Best Buy will close 250 cell phone stores. JC Penney, after closing more than 140 stores in 2017, will be shutting down one of its distribution centers and eight more stores nationwide in 2018. Michael Kors will close between 100 and 125 of its retail stores over the next two years.

The list goes on, but suffice to say, we believe the retail apocalypse is happening.

•••••

Looking at next steps and finding value

Looking away from all the turmoil, we remain focused on what we see as incredible value—and opportunity—for our investors going forward. Our long portfolio remains highly concentrated on a set of companies we believe are best positioned to lead us, long-term, into the future.

These are companies with visionary leaders who are determined to find value for their customers—not necessarily with pleasing the short-term whims of Wall Street analysts. The beauty of focusing, and truly understanding a business, is that it helps provide confidence in the potential of turmoil.

This may occasionally, as it has in the past, lead to short-term volatility. But we are investing in businesses whose value on a day-to-day basis is relatively unchanged. That said, they seem to be growing at compounding rates and in impressive fashion.

Since 2012, I’ve been impressed by Netflix’s customer-focused leadership, but more recently I’ve been blown away by their ambitious content plan.

In 2018, Netflix plans to release 80 original films—more films than the major studios combined. The streaming giant now has about 118 million subscribers who pay about ten bucks a month to access thousands of shows and movies on demand. As a customer, this value proposition is stunning, and it’s no wonder Netflix has thrown the Hollywood studio model into chaos: The company has amassed enormous troves of viewership data, their programming allows for adaptable customer behavior (i.e. binge watching), and they don’t have to battle the capricious theatrical “windowing” that can bust studio marketing budgets with little return.

As of late March, Netflix has nearly reached the market value of Disney—and I will not be surprised when they pass the 95-year old storied studio in market value. After all, this is what disruption looks like: upstarts surge onto the scene with brutal consequences for incumbents.

On the electric car front, we continue to watch the decline of the Internal Combustion Engine (ICE)—and we remain bullish on the long-term prospects for the next phases of the electric vehicle revolution.

Despite the volatility in price, Tesla had an incredibly exciting quarter: The Gigafactory 1 in Nevada, where Tesla produces battery cells as well as its own Model 3 battery packs and drive units, is operational and humming. Gigafactory 2 is being built in Buffalo. The Supercharger network is expanding rapidly. As of this writing, the company has 1,191 Supercharger Stations with 9,184 Superchargers around the world.

But perhaps the most exciting element of Tesla is the Model 3. Despite production delays—which are not unexpected—Tesla’s Model 3 is potentially the biggest game-changer yet, in our opinion. The last time I’ve seen this much excitement for a new product was when Apple launched the iPhone. For Tesla, the Model 3 is their iPhone moment. (On a personal note, I have been enjoying driving my new Model 3, which arrived in early 2018. It’s an amazing car, and when consumers get a chance to get behind the wheel, they’ll realize very quickly that there is no going back to an ICE vehicle.)

At the end of Q1, Tesla reached a production target of 2,000 Model 3 vehicles per week, making it the new #1 electric car in the United States. There is an extremely high level of speculative headlines on Tesla—much of it negative. And that’s not surprising. There is a lot of money and power at stake here – this will always attract naysayers. We experienced the same backlash upon our investments in Amazon with a focus on AWS. If we are correct that cars are indeed going electric, Tesla is in a position to be uniquely successful. Companies at this stage require more complex valuations, and my models have reflected the various possibilities that could result. We really like this investment opportunity.

•••••

ESG Investing at Nightview Capital: Where socially-responsible investing meets technological disruption

As Nightview Capital grows, we want to make sure that new investors are fully aligned with our social and environmental philosophy. So this week, we are publishing a manifesto of sorts about Nightview Capital’s approach to Environmental, Social And Governance investments. You can read the specifics in the PDF at the end of this letter.

We don’t view ESG missions simply as a token symbol of responsibility. Our ESG investment commitment is also born out of simple economic reality: We believe going “green” is good for business.

The value proposition of a cleaner planet with responsible businesses is a better value for its inhabitants, and in the long-term, the customer value proposition always wins: Just like mainframe shifted to cloud, or retail has shifted online, the transformation to clean energy will be driven by consumer demand.

•••••

Next steps—and looking ahead

As always, our goal is to return multiples on investor capital—tax efficiently—over a long time-horizon. Rather than attempting to squeeze returns out of companies through financial engineering or temporary performance increases, we remain focused on the long term, and investing in great businesses.

I’d like to personally thank you for being our client, and if you have any questions, please do not hesitate to reach out.

Sincerely,

Arne Alsin

Disclosures:

This has been prepared for information purposes only. This information is confidential and for the use of the intended recipients only. It may not be reproduced, redistributed, or copied in whole or in part for any purpose without the prior written consent of Nightview Capital.

The opinions expressed herein are those of Nightview Capital and are subject to change without notice. This is not an offer to sell, or a solicitation of an offer to purchase any fund managed by Nightview Capital. Such an offer will be made only by an Offering Memorandum, a copy of which is available to qualifying potential investors upon request. This material is not financial advice or an offer to sell any product. Nightview Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Past performance is not indicative of future results. Returns are presented net of investment advisory fees and include the reinvestment of all income. Nightview Capital Management, LLC (Nightview Capital) is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Nightview Capital including our investment strategies and objectives can be found in our ADV Part 2, which is available upon request. WRC-18-04.